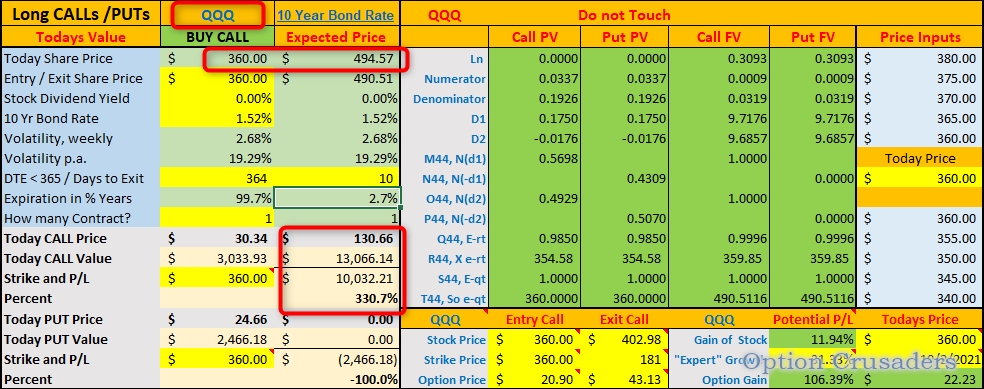

Make sure that you understand all four previous blogs. They are fundamentally important to this trading tactics.

bear-call-credit-spread-histogram-3_20

Additions

I introduced the True Average and the Average True Range, ATR, into the equation. To calculate the True Range is easy, please look it up on the web. For EVERYTHING you need there is a exact equation somewhere in the EXCEL websites. Guaranteed. I am not providing this here. I just explain the concept in detail as a guideline.

Having the weekly TR you also can calculate the Average True Range, the ATR.

I calculate the ATR only off 4 weeks. That is the average of one month movement. It is not so much of a difference to the typical 14 day ATR but for me I want the empathize the immediate past. Do as you see fit.

These data are also collected from Yahoo and should already be part of the download.

We already calculated the Average Return per week, our Pos Avg Return, the worst case scenario of 100% uptrend! And we multiplied it with the occurrences in the data set, here 53.05% of the weeks. The amount of weeks that the underlaying is actually up by incorporating the downturns from the dataset. This is our mean average return.

Now that we have three averages, the worst case, the mean case, and the ATR I summed them all up and averaged them. This is what I call the BINGO NUMBER, in yellow circle. This is my STRIKE PRICE.

= AVERAGE(237.35 + 246.80 + 235.50)

= 239.89

So far the Bingo Number is slightly below the 2StdDev. So the Entry can be 2StdDev. If the Bingo number comes out above the 2StdDev take that as an entry.

What is the reason behind these calculations?

These calculations give us the best probable setup for our SHORT CALL Option that still makes sense for a better ROC. For the Return On Capital Ratio, the credit in relation to the collateral capital of the trade you have to come up with, we want to go as close as possible to the current price, "ATM", At The Money. This gives the highest CREDIT.

But also we want to stay as far away as possible from the current price of the underlaying, Out of The Money, OTM, to not hit the Strike. The calculated Bingo Number will be the STRIKE Price of the trade and brings Risk/Reward into balance.

All over all it stays 2 Standard Deviations away and hence has a trigger rate of about 10.7%. The ROC is about 6.5-7.5% depending on volatility and Yield Rate.

ROC Considerations.

The IWM is creating more ROC than the QQQ and the SPY. The two latter ones are close to 5% with this setup. The DIA (Dow Jones Industrial Average) runs under 2% with this setup and hence is completely excluded.

In our example we calculate ROC as

144 -(2 x 10.95) / 1,866.95 = 6.5%.

122.10 / 1,866.95 = 6.5%

Dont forget to substract 2 x FEES for the full turnaround.

With a 10% chance of getting hit and we reserve $50 for max losses per contract due to volatility and treasury yields (just close the trade at Strike Price) we have to substract this from the net ROC.

We might have

45 winners at net of $122.10, times 45 = $5,500

5 losers at 4 x $50.00, times 5 = $1,000

Net gain in one year of $4,500

The gain percentage would be 4,500 / 7,600 = 60%

If you can pull this off every hedge fund manager will hire you.

WHY?

Because your Kelly Criterion would be

Everything above 2.00 profit per Dollar is exceptional. And everything about 20% trade size is exceptional.

You are free to add any ZEROS to this game. We are not here to calculate hard numbers but to give examples and percentages.

Take a trade per week and do it 50 weeks a year! This will double your account.

Trade Entry

We enter the trade NOT to follow a trend up or down. We dont pick bottoms or tops! We try to get in, in the middle. For that reason we wait for two green (blue) candles and enter on the third day after 30 minutes of the Opening. We try to jump in on the top then, which occurs roughly at 0900-1000 NY Time. Let the rush go and try to sell at the top. Thats it! If that doesnt work out we enter anyways. Dont worry.

Why do we try to get in at the middle?

We know the swings in that stock and we calculated the deviations and when you look at the swing pattern and the technicals we see that after a few days up there are coming a few days down! These down days decay the Days To Expiration, Theta of the Option trade and hence it will have to come out from the bottom. We want to take advantage of this and further add to our odds. We want to own the bank in the casino. We are not here to play! Take a look at this image and you know what I mean.

Another reason for letting two green candles pass is that in an upward move CALLs become more expensive and hence give us a bigger credit. This is important. If you follow the stock you will notice that.

Definition of two Green Candles

- Two bull candles

- One bull candle and a gap n' crap with a doji

The third last candle was a bull candle and hence valid, the next candle was a red DOJI and it gapped open, which means there was a lot of after market trading and I count this as a bull candle for the purpose of this exercise. You want to sell into the uptrend. So we entered on the last candle.

Daily Charts

5 Minute Charts

Days to Expiration

We chose 30 DTE. I was considering 45 DTE since there is more money for a credit to get, true, but I decided for a monthly roll over and my calculations run on a 4 week base for some numbers. This is all up to ones liking.

Exit Trade

- Let the Trade expire and keep the CREDIT.

- If the trade runs against us close at Strike Price! Remember, you get the credit up front and when you are down by the total amount of your credit you are at Break Even only. This means at Strike your OPEN P/L should be negative CREDIT RECEIVED. You close and just give back the credit. There should not be any losses. Except commissions and fees.

- You might endure some losses due to volatility and yield rate. That amount might vary some from the BE.